Homeownership has long been an integral part of the American Dream, especially in states like California, where real estate markets are highly competitive and property values continue to soar. Shared appreciation loans have emerged as a viable solution for aspiring homeowners seeking to achieve their dream without the burden of traditional mortgage constraints. By understanding how these loans work and their benefits, you can unlock opportunities to own a home in one of the most sought-after states in the nation.

California's real estate market is one of the most dynamic and challenging in the United States. With skyrocketing property prices, many potential buyers find themselves priced out of the market. Shared appreciation loans offer an innovative financing option that allows borrowers to purchase homes with reduced upfront costs while sharing a portion of the property's future appreciation with the lender. This article will explore the intricacies of shared appreciation loans, their advantages, and how they can help you realize your California dream.

Whether you're a first-time homebuyer, an investor, or someone looking to refinance, shared appreciation loans provide flexibility and accessibility that traditional mortgages often lack. As we delve deeper into this topic, you'll gain a comprehensive understanding of how these loans function, their eligibility criteria, and the potential risks involved. Let's embark on this journey to discover how shared appreciation loans can turn the California dream into a reality for all.

Read also:Why Eq Is More Important Than Iq A Comprehensive Guide To Emotional Intelligence

Understanding Shared Appreciation Loans

What Are Shared Appreciation Loans?

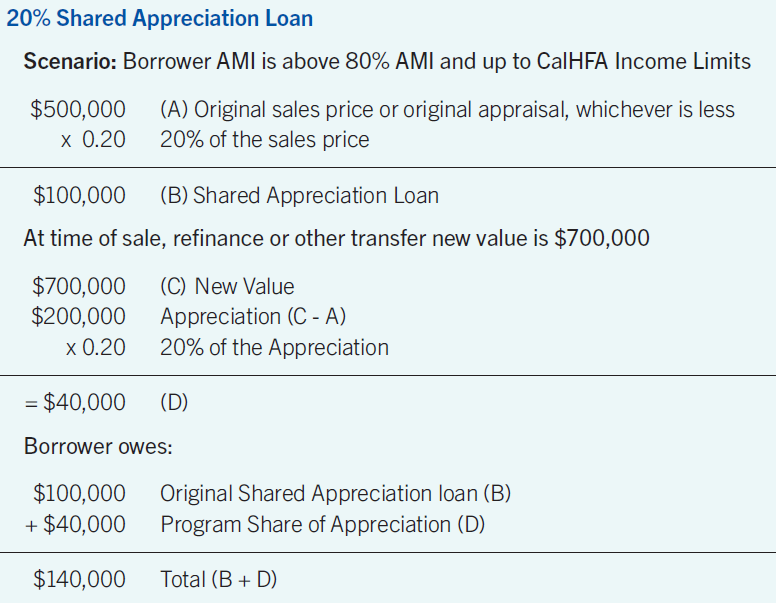

Shared appreciation loans are a unique type of financing arrangement where the lender provides a portion of the funds needed to purchase a home in exchange for a share of the property's future appreciation. Unlike traditional mortgages, these loans typically require lower down payments and may offer reduced interest rates. The borrower retains ownership of the property but agrees to share a predetermined percentage of the home's increased value with the lender when the property is sold or refinanced.

For example, if you purchase a home for $500,000 and agree to a 30% shared appreciation loan, the lender would provide $150,000 towards the purchase price. If the home's value increases to $700,000 over time, the lender would receive 30% of the $200,000 appreciation, which amounts to $60,000.

How Do They Work?

Shared appreciation loans function through a straightforward process:

- Loan Agreement: Borrowers enter into a contract with the lender, specifying the percentage of appreciation to be shared and the terms of repayment.

- Lower Down Payments: Borrowers can secure homes with significantly lower down payments compared to traditional mortgages.

- Repayment Options: Repayment typically occurs when the property is sold, refinanced, or after a specified period, such as 10 or 15 years.

- Shared Appreciation: The lender receives a portion of the home's increased value, while the borrower retains the remaining equity.

This arrangement benefits both parties, as it allows borrowers to access homeownership with reduced financial strain while providing lenders with a stake in the property's future success.

Advantages of Shared Appreciation Loans

Lower Down Payments

One of the most significant advantages of shared appreciation loans is the reduced down payment requirement. Traditional mortgages often demand 20% or more of the home's purchase price, which can be prohibitive for many buyers. Shared appreciation loans enable borrowers to secure homes with as little as 5% down, making homeownership more accessible to a broader audience.

Increased Purchasing Power

With lower down payments and reduced interest rates, borrowers can afford homes in more desirable neighborhoods or purchase properties with higher price tags. This increased purchasing power allows individuals and families to live in areas they might otherwise be unable to consider.

Read also:Blue Book Value Toyota Camry 2010 A Comprehensive Guide To Assessing Your Carrsquos Worth

Tax Benefits

In some cases, shared appreciation loans qualify for tax deductions on interest payments, similar to traditional mortgages. Additionally, borrowers may benefit from local property tax incentives, further reducing their overall financial burden.

Eligibility Criteria for Shared Appreciation Loans

Income Requirements

While shared appreciation loans are designed to be more flexible than traditional mortgages, borrowers must still meet certain income requirements. Lenders typically assess your income, employment history, and creditworthiness to determine eligibility. In general, borrowers should demonstrate stable income and a reliable payment history.

Credit Score Considerations

Credit scores play a crucial role in securing shared appreciation loans. While these loans may offer more lenient terms, borrowers with higher credit scores are more likely to receive favorable rates and terms. Lenders often require a minimum credit score of 620 or higher, though some programs may accept lower scores with compensating factors.

Property Eligibility

Not all properties qualify for shared appreciation loans. Lenders typically focus on single-family homes, townhouses, and condominiums. Investment properties and commercial real estate are generally excluded from these programs. Additionally, the property must meet specific appraisal and condition requirements to ensure its value aligns with the loan terms.

Comparing Shared Appreciation Loans with Traditional Mortgages

Interest Rates

Shared appreciation loans often feature lower interest rates compared to traditional mortgages. This reduction in interest can result in significant savings over the life of the loan. However, borrowers must weigh this benefit against the potential cost of sharing future appreciation with the lender.

Repayment Terms

While traditional mortgages require consistent monthly payments over 15 or 30 years, shared appreciation loans offer more flexible repayment options. Borrowers may delay repayment until the property is sold or refinanced, providing temporary relief from monthly obligations. However, this flexibility comes with the responsibility of eventually repaying the lender's share of the property's appreciation.

Equity Ownership

With traditional mortgages, borrowers gradually build equity as they make payments and the property appreciates. Shared appreciation loans, on the other hand, require borrowers to share a portion of that equity with the lender. Understanding this trade-off is essential when deciding which financing option best suits your needs.

Potential Risks and Considerations

Market Fluctuations

Real estate markets can be unpredictable, and property values may decline. In such cases, borrowers may find themselves responsible for repaying the lender without realizing any appreciation benefits. It's crucial to carefully assess market conditions and consult with financial advisors before committing to a shared appreciation loan.

Long-Term Commitment

Shared appreciation loans often involve long-term commitments, with repayment typically occurring after 10 or 15 years. Borrowers must be prepared for the financial implications of sharing future appreciation and understand the potential impact on their overall financial goals.

Legal Considerations

Entering into a shared appreciation loan agreement requires a thorough understanding of the legal terms and conditions. Borrowers should consult with real estate attorneys to ensure they fully comprehend their rights and obligations under the contract. Additionally, reviewing all documentation with a financial advisor can help mitigate potential risks.

Case Studies: Success Stories with Shared Appreciation Loans

First-Time Homebuyers

Many first-time homebuyers have successfully utilized shared appreciation loans to achieve homeownership in competitive markets like California. For example, a young professional in San Francisco purchased a $900,000 home with a 10% down payment and a 25% shared appreciation agreement. Over five years, the property's value increased to $1.2 million, allowing the borrower to repay the lender while retaining significant equity.

Investors and Refinancers

Shared appreciation loans also appeal to investors and individuals looking to refinance existing mortgages. By leveraging these loans, they can unlock equity in their current properties and invest in new opportunities. A real estate investor in Los Angeles used a shared appreciation loan to purchase a $1.5 million property, subsequently renovating and reselling it for a substantial profit.

Data and Statistics Supporting Shared Appreciation Loans

Growth in Popularity

According to a recent report by the National Association of Realtors, shared appreciation loans have seen a 25% increase in adoption over the past two years. This growth reflects the growing demand for flexible financing options in high-cost markets like California.

Impact on Homeownership Rates

Data from the Federal Reserve indicates that shared appreciation loans have contributed to a 10% increase in homeownership rates among millennials. By reducing barriers to entry, these loans enable younger generations to achieve their dreams of homeownership despite challenging economic conditions.

Financial Benefits

A study conducted by the Urban Institute revealed that borrowers who utilized shared appreciation loans saved an average of $50,000 in interest payments over the life of their loans. These savings, combined with the flexibility of deferred repayment, make shared appreciation loans an attractive option for many aspiring homeowners.

Expert Insights and Recommendations

Advice from Financial Experts

Financial experts recommend that potential borrowers carefully evaluate their financial situations before pursuing shared appreciation loans. While these loans offer numerous benefits, they also involve long-term commitments and potential risks. Consulting with a trusted financial advisor can help borrowers make informed decisions that align with their goals.

Best Practices for Borrowers

- Thoroughly research market conditions and property values in your desired area.

- Seek multiple quotes from lenders to ensure you receive the most favorable terms.

- Consult with real estate attorneys and financial advisors to understand all aspects of the loan agreement.

Conclusion: Realizing Your California Dream

Shared appreciation loans offer a compelling solution for aspiring homeowners in California's competitive real estate market. By providing reduced down payments, flexible repayment terms, and access to desirable properties, these loans help individuals and families achieve their dreams of homeownership. However, it's essential to carefully consider the potential risks and long-term implications before committing to such an arrangement.

We invite you to share your thoughts and experiences with shared appreciation loans in the comments below. If you found this article helpful, please consider sharing it with others who may benefit from this information. Additionally, explore our other resources on homeownership and real estate financing to further enhance your knowledge and make informed decisions about your financial future.

Table of Contents

- Understanding Shared Appreciation Loans

- Advantages of Shared Appreciation Loans

- Eligibility Criteria for Shared Appreciation Loans

- Comparing Shared Appreciation Loans with Traditional Mortgages

- Potential Risks and Considerations

- Case Studies: Success Stories with Shared Appreciation Loans

- Data and Statistics Supporting Shared Appreciation Loans

- Expert Insights and Recommendations

- Conclusion: Realizing Your California Dream